Is the American Dream of Homeownership Dead?

The Shift No One Wants to Talk About

Is the American Dream still alive, or have young adults quietly begun to abandon it, especially when it comes to buying a home? To understand where the economy is heading… you don’t start with Wall Street. You follow the food.

The food industry has always had an uncanny ability to sense the nation’s financial pulse long before headlines catch up.

During my years with McDonald’s, I had a front-row seat to this reality. What most people see as a burger chain is, in truth, a real-time economic dashboard. From farm to table, every variable is tracked sales volume, product mix, average customer spend, year-over-year trends, and the subtle but powerful shift from premium choices to value-driven decisions.

And when those patterns change… it’s never random. It’s behavioral. It’s economic. It’s predictive.

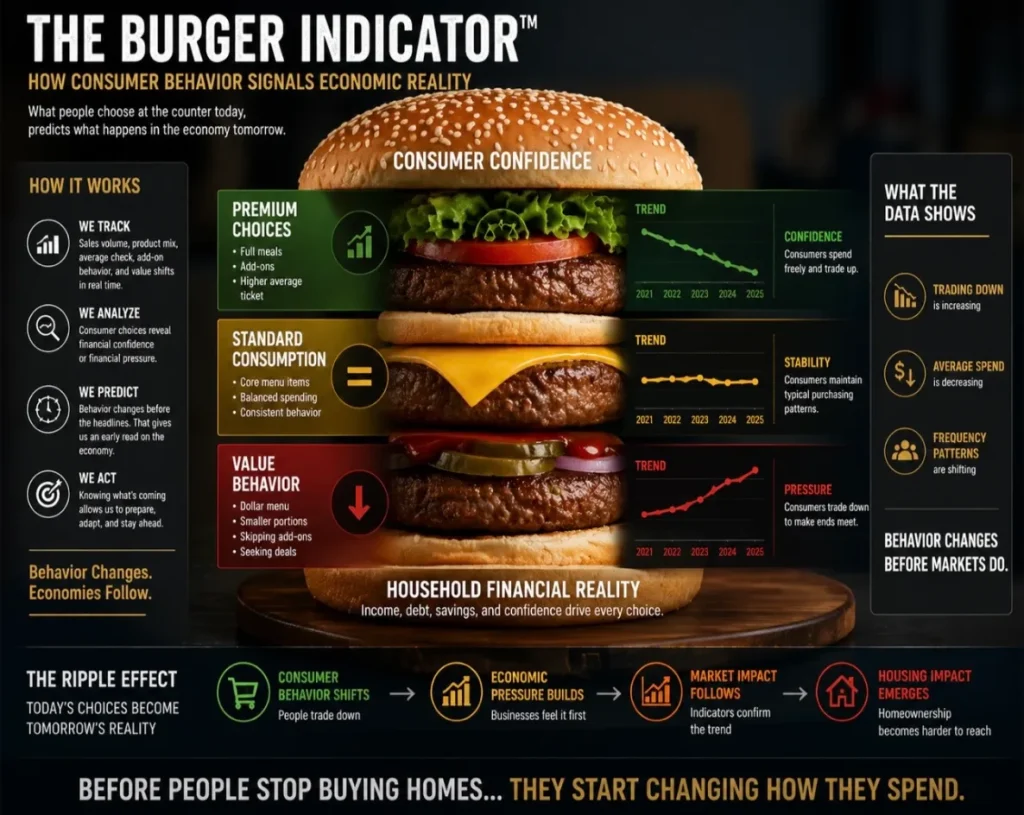

THE BURGER INDICATOR

Inside the system, we called it: The Burger Indicator. And it was shockingly accurate. When consumers began trading down choosing smaller meals, lower-priced items, or skipping add-ons altogether it signaled something deeper: Pressure was building. Not in the markets first but in households.

THE SHIFT before people stop buying homes… First they start adjusting how they live. It doesn’t happen all at once, it happens quietly, gradually, almost invisible at first. They cut back on discretionary spending, delaying major decisions. They pause, reassess, and begin to prioritize flexibility over long-term commitment. What used to feel like a natural next step buying a home now feels like a calculated risk. Monthly budgets get tighter. Down payments feel heavier and the margin for error shrinks.

Over time, behavior begins to change. First-time buyers are entering the market later than ever before, not because they lack ambition, but because the pathway has become more complex and less forgiving. Many are choosing mobility over ownership, valuing the ability to move, adapt, and respond to opportunity. Others are becoming more intentional, shifting their focus toward debt freedom, liquidity, and financial independence before ever considering a mortgage. The definition of “success” starts to evolve not anchored solely in ownership, but in control, flexibility, and resilience. The dream doesn’t disappear, it’s redefined. It becomes more strategic, more cautious and often delayed. What was once an expectation becomes a question. What was once assumed becomes something that must be carefully planned and well defined. The shift isn’t away from homeownership entirely, it’s a shift in timing, priorities, and perception.

THE PARADOX and yet… the desire hasn’t gone away. Beneath all the adjustments, hesitation, and redefinition, the fundamental pull toward homeownership remains as strong as ever. At its core, owning a home still represents something deeply meaningful; stability, autonomy, and a tangible stake in the future. It’s not just emotional, it’s calculated. Homeowners still hold a massive advantage, and the numbers make that clear. The average homeowner has roughly $430,000 in housing-related wealth, compared to just $10,000 for renters. That gap isn’t incremental, it’s exponential. It reflects years of principal paydown, asset appreciation, and leveraged growth that renters simply don’t capture. It’s the difference between participating in the financial ecosystem or watching it from an outside perspective.

That’s the paradox. At the very moment homeownership feels like it’s the most difficult to attain, and its value becomes even more pronounced. The barriers to entry have gone up, but so has the long-term impact of getting in. The dream hasn’t faded, it’s intensified. People still want it, they still see it as a cornerstone of financial progress and personal freedom. So the dream remains alive, just further out of reach for many. Not because it no longer matters, but because navigating the path now requires more awareness, more strategy, and a deeper understanding of how the system truly works. Having the right tools to financially navigate the system is a significant advantage to expedite liabilities and build assets.

Fast-Forward to 2026

A calm surface… hiding deep currents. At first glance, today’s market appears stable-but the underlying data tells a very different story. The Federal Reserve holds steady on interest rates. Economists expect that trend to continue. On the surface, stability. But beneath it, the market is recalibrating. Home prices are leveling. Inventory is rising. Sales activity is slowing. A shift is underway. But “balanced” doesn’t mean accessible. Affordability remains strained. Even minor rate changes continue to sideline buyers.

THE MARKET HAS SHIFTED while homeownership becomes harder to reach… the rental market is accelerating. New developments are rising everywhere. Supply is increasing. Vacancy may tick up-but demand is keeping pace. Rents continue to climb just more gradually. And beneath it all… A deeper shift is taking place. More Americans are renting longer-not by choice, but by necessity. This isn’t temporary.It’s generational. The path has changed. The timeline has stretched. The outcome is no longer guaranteed.

THERE’S A BETTER WAY

Not a new opinion. A new technology system. The market changed. The system most people follow… didn’t.

METHODOLOGY

THE DECISION

You’ve seen the data. You’ve seen the shift. Now see your numbers.

WHAT’S YOUR DEBT FREE NUMBER?

Discover the exact month and year you can eliminate your debt—

and how much interest you can cancel along the way.

Schedule your complimentary analysis. Leave your wallet at home.