Grow & Protect Wealth

The Retirement Gamble

Brother “A” & Brother “B”

The risk no one talks about At Method Analytics, everything begins with one truth. Time is your most valuable asset. Yet most financial strategies are not designed to protect your TIME. They are designed to follow a path, often without fully considering risk, taxation, or long term efficiency. Our full service Debt to Wealth philosophy is built to change that. Our agency incudes licensed and insured experts, as a firm we focus on positioning your money out of harm’s way, minimizing or eliminating future tax consequences where possible, and creating a strategy that is designed to adapt as life happens.

Whether you have retirement accounts from past employers or are currently contributing to a traditional plan, we analyze your entire financial picture to determine how it is truly working and where it can be improved. The goal is simple. Maximize what you keep, create income that lasts, and give you the ability to live life on your terms with clarity, confidence, and dignity. If you leave your future to chance, you are not planning, you are gambling. Most people are not failing because they lack discipline. They are following a system that was designed to be followed, not optimized. A system built on doing what everyone else does, without questioning how it truly works. And that creates a risk most people never see. Not market risk. Not investment risk. Control risk. Because when your future depends on rules you do not control, outcomes you cannot predict, and tax rates that are not fixed, you are exposed in ways most people never consider.

A Tale of Two Brothers

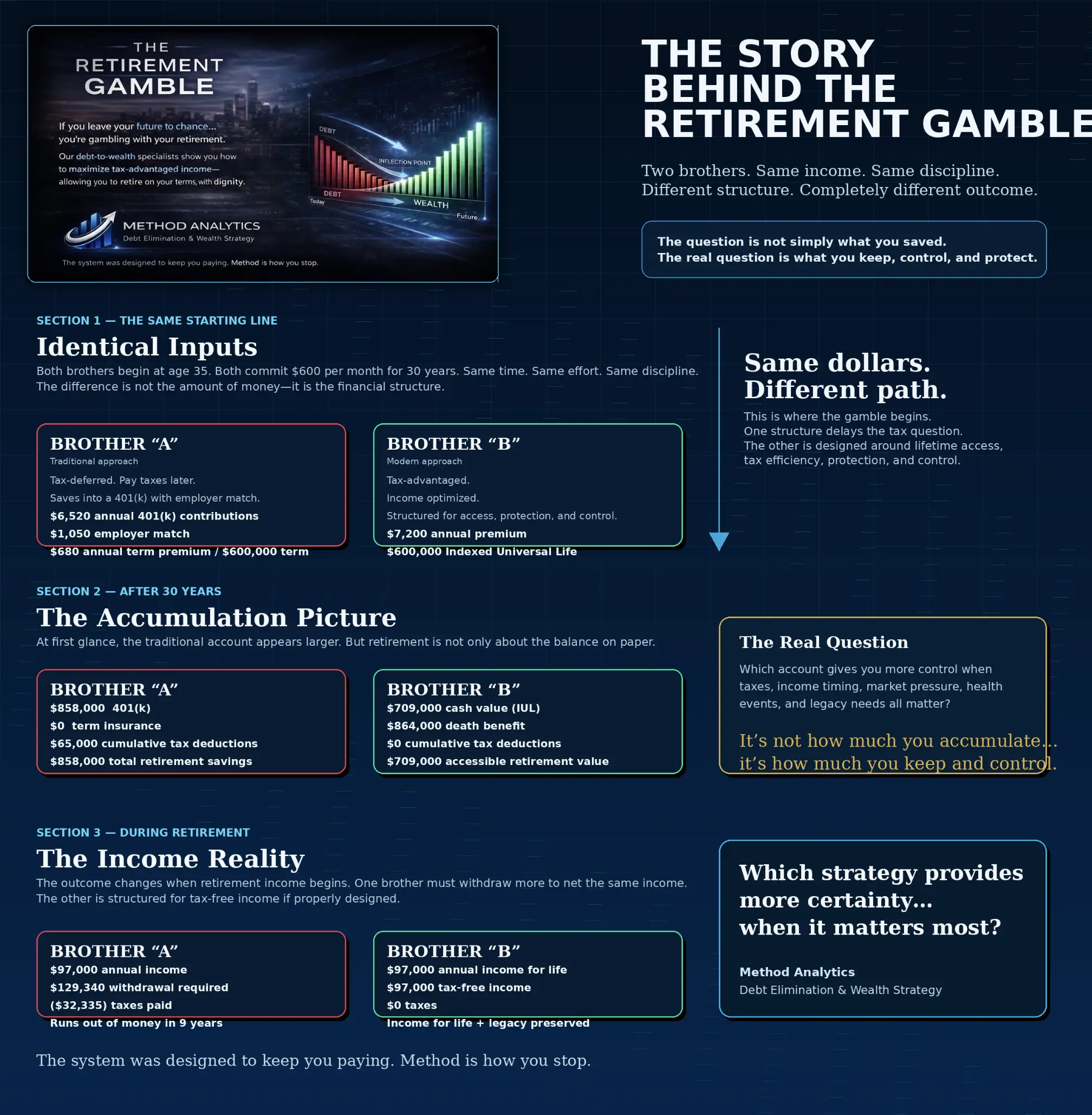

Two identical decisions, or so it seems. Both brothers are 35. Both save $600 per month. Both earn 8% over time. Same money. Same discipline. Same timeline. At first glance, the outcome should be identical. But it is not. Identical Inputs. Different Structure Brother A follows the traditional path. A static, linear approach. His strategy is tax deferred, meaning he agrees to pay taxes later under whatever rules exist at that time. He contributes to a 401(k), carries term insurance for protection, and depends on withdrawals in retirement that are exposed to taxation and market timing. He is not just exposed to market risk. He is exposed to future tax policy. There are no guarantees on what those tax rates may be, how they may change, or how much of his income he will ultimately keep.

Brother B follows the Method Analytics approach. A dynamic, engineered system. His strategy is structured with tax efficiency in mind from the beginning. His income is optimized, not assumed. Protection and growth work together. His plan is built using the Method Analytics Financial GPS, a system that continuously recalculates and adjusts in real time as life happens, ensuring he remains on the most efficient path forward. What Makes the Difference This is not about picking better investments. This is about structure, sequencing, and control. Method Analytics is a precision engineered financial system designed to dynamically optimize cash flow, minimize unnecessary interest and tax exposure, and determine the fastest, most efficient path forward. It continuously recalculates as variables change, ensuring every decision is aligned with the optimal outcome, precise to the penny. Because in finance there is not more than one optimal path. There is one. Everything else costs you time and money.

Results After 30 Years Brother A accumulates $858,000. His money is tax deferred, not tax free. His term insurance provides no living value. His outcome is $858,000 before taxes, with future tax exposure still unknown. What he ultimately keeps depends on decisions that have not yet been made. Brother B has $709,000 in accessible cash value and an $864,000 protected death benefit. His plan is structured for tax efficiency, control, and flexibility. His outcome is not just accumulation. It is accessible wealth, protection, and greater certainty over how and when that money is used. It is not about what you accumulate. It is about what you keep, what you control, and what you can actually use.

Results During Retirement Brother A generates $97,000 of annual income but must withdraw $129,340 to do it. His income is taxable. If tax rates increase, his required withdrawals increase with them. Over time, the system becomes less efficient and eventually runs out. Brother B also generates $97,000 of annual income. His income is structured to be tax efficient if designed properly. He does not require excess withdrawals. His income is designed to last with greater predictability and control. One plan depends on future assumptions. The other is built with control in mind.

Why This Happens. Most financial strategies are static. They do not adjust. They do not optimize. They do not account for changing conditions such as tax policy, income shifts, or life events. Method Analytics does. It functions as a Financial GPS. Not a map. Not a projection. A dynamic system that continuously recalculates, adjusts for income, expenses, and life events, and identifies the most efficient path forward at all times. Because the shortest path is not always obvious. But it is always mathematical.

What Is Indexing Indexing is a strategy designed to capture growth while protecting against loss. When the market rises, you participate in that growth. When the market declines, your principal is protected. Gains are locked in, creating a stronger compounding foundation over time. This is how you get the safety of protection with the growth potential of the market. Which path would you rather be on?

Final Thought

Compound interest is the eighth wonder of the world. He who understands it earns it. He who does not pays it. Albert Einstein What’s Your Debt Free Number? The Month and Year you will claim Financial Independence. Using Method Analytics, we can show you the exact month and year you can become debt free, how much interest you can eliminate, and how to redirect that money toward building wealth. No guesswork. No pressure. Just math.

Be Prepared.

Preparation is not about fear. It is about responsibility. It is about control. Life does not wait until you are ready. Every day, we are one day older. Every day, we have one less day. Time continues forward whether we have a plan in place or not.

Obituaries are filled with people whose lives ended sooner than expected. Not because they planned for it, but because life does not always follow a predictable timeline. Serious illness and medical expenses remain one of the leading causes of financial collapse for families. It is not just the emotional toll, it is the financial impact that follows, often unplanned and overwhelming. Statistics show that children experience loss far more often than most people are willing to consider. Families are disrupted. Plans are interrupted. Lives change in an instant.

This is not about expecting the worst. It is about being prepared before the need. Because when there is no plan, decisions are made under pressure. And pressure leads to costly outcomes, financially, emotionally, and in TIME.

Planning now for tomorrow creates a different reality. It allows you to move with clarity instead of urgency. It protects not just your finances, but the people and the life you have worked to build.

Without a system, most people drift. They earn, they spend, they manage, but they do not optimize. And over TIME, that inefficiency compounds. Not just in dollars, but in years.

Preparation changes that.At Method Analytics, preparation is engineered. Using advanced, dynamic financial technology, we help you see exactly where you are, where you are going, and how to get there in the most efficient way possible. The goal is not just to build wealth. It is to create certainty. To create structure. To ensure that no matter what life brings, you are positioned, protected, and prepared.

Because the future is not guaranteed.Being prepared for it is a choice.

Engineered. Precise. Dynamic. Proven.